Your task performs a vital role in your capability to score a home loan. Once you submit an application for financing, their financial tend to assess your own employment history to make sure you had a supply of constant earnings for at least a couple of years. Exhibiting that you are financially with the capacity of trying to repay that loan is an essential part of getting approved.

Additional employment brands have a tendency to affect your house application for the loan. But before we talk about one to, let us review a few of the things taken into consideration when you submit an application for home financing.

More loan designs need sizes from down money. Out of a great lender’s direction, with a considerable deposit will require less cash are borrowed, ergo reducing the chance thought from the bank.

It is recommended that homeowners have sufficient spared to put off during the minimum 20% of house’s really worth towards the mortgage to quit Financial Insurance rates. But not, this isn’t a requirement. Such, Va and you may USDA* fund not one of them any deposit whatsoever. (A lot more charge can get pertain.)

Financing Term

The word, otherwise duration, of mortgage, ’s the amount of time you have to pay off the loan. Shorter-identity money will often have straight down interest levels and lower full costs, however, high monthly payments. After evaluating debt suggestions and you can long-identity needs, the financial can get strongly recommend financing distinct from everything you got expected.

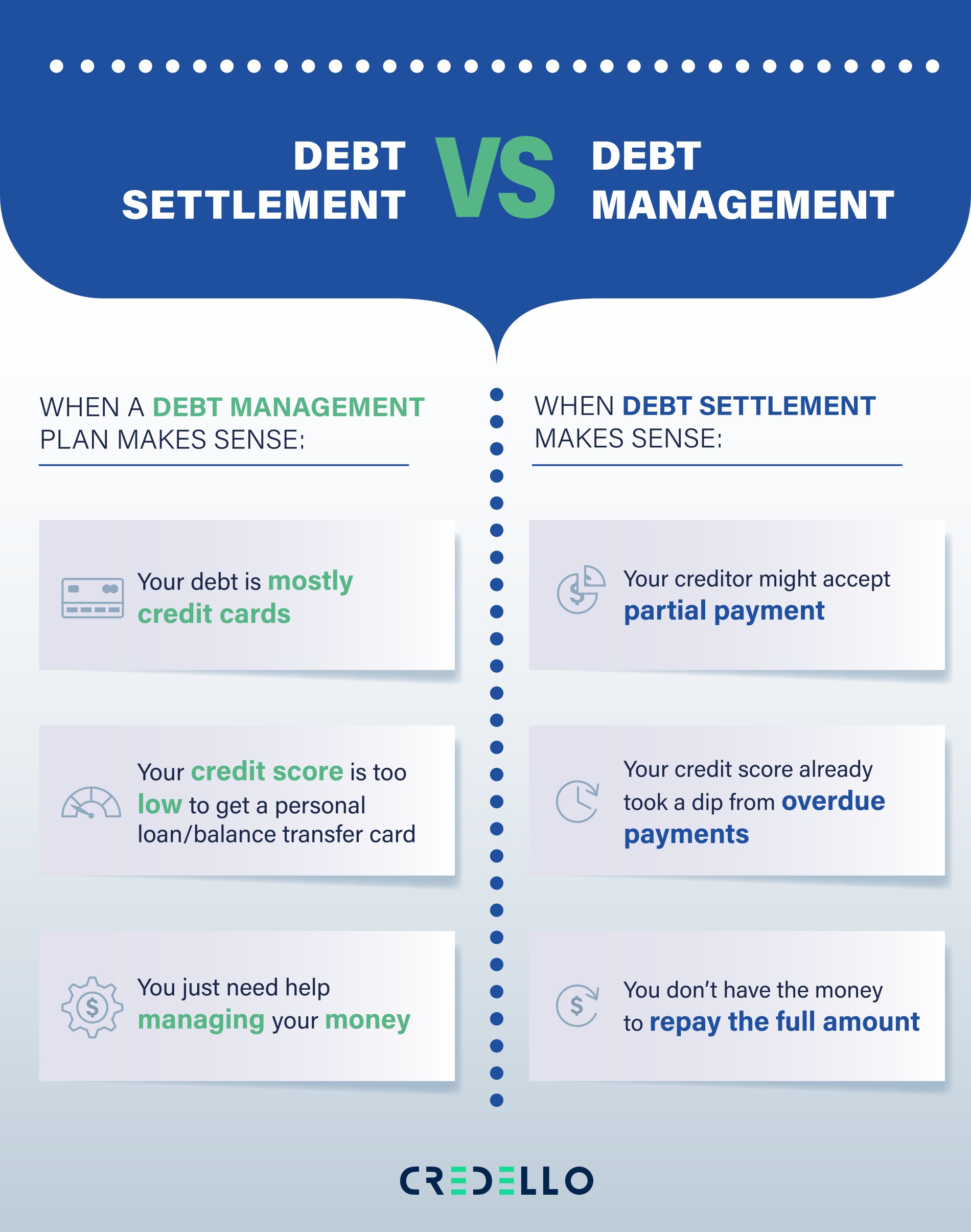

Credit rating

Your credit score is a simple-to-see manifestation of the creditworthiness and you may capacity to pay off their financial. For those who have a track record of later money, otherwise worse, forgotten multiple days off money, your own rating usually echo that it. If you find yourself you’ll find loans one deal with a reduced credit score, there are constantly most costs that really must be paid down.

Debt-to-Income Ratio

Your DTI was counted by the monthly personal debt repayments divided from the the terrible month-to-month income. That it matter is a sure way lenders level what you can do to cope with the newest payments you make every month to settle the money your enjoys lent. In the event the DTI proportion is just too highest, you need an excellent co-debtor to help you get a property.

Employment Records

It is not about precisely how far you make, however, regardless of if your revenue was stable. Proof of a steady income source is vital to a lender.

If for example the business history reveals a pattern off moving from just one team to a higher or tall holes on your own employment, this is often a major warning sign to help you a manager. Exactly what if you don’t really works a timeless full-time jobs?

Doing work a timeless 9-5 employment is almost certainly not the facts. To own price professionals, advertisers, and you may lots of other types of personnel, your house mortgage process may look a small additional.

Temp Workers

Employing short term professionals is a popular decision around the of a lot performs industries as well as It, Recruiting, Customer service, and much more. Exactly how really does a good temp employee tell you a consistent income if work change appear to?

In the event the a good co-debtor is www.paydayloancolorado.net/victor/ on the mortgage, your lender will get think the a job record to-be legitimate adequate in order to the borrowed funds. But not, you happen to be asked to incorporate a lot more data that demonstrate past and ongoing work.

Deal Pros

Although some builders is viewed as providers staff, almost every other contract employees are said to be freelance or spend-as-you-wade team. These earnings is seen as high risk from the specific lenders, given that they there’s no make sure that another business can come afterwards.

Similar to temp workers, developed personnel may be wanted more data files to show the work has been regular prior to now and will keep since like.

Self-Operating

Lenders will ask for evidence of a job that have pay stubs and you can W2 models. Since a personal-functioning debtor won’t have such data, they generally have to provide as much as a couple of years out of income tax yields. Although not, specific loan providers render financial report fund.

On PRM, we recognize the necessity of having choice applications to fit the fresh requires of your subscribers. The fresh PRM Bank Report Financing has the benefit of:

- Repaired and you will adjustable prices

- Three additional bank statement choices useful for income computation**:

- a couple of years out of business bank statements

- 2 years from personal bank statements

- 12 months out-of personal bank statements

- Mortgage number offered around $2.5 billion

- Solitary Nearest and dearest Houses, also Condos, Non-Warrantable Apartments, and you will Townhomes

- Proprietor Filled and you may 2nd Family

- Interest-only option available

Obtaining a home loan should be a stressful procedure. Our company is right here to really make it easier for you. Get in touch with home financing Advisor for additional information on the new applications and you can affairs you can expect.